Buying New Launch Condos as A Trust

In a recent post, I talked about how parents are buying private property in a trust. The talk is that the parents did it as a means to avoid Additional Buyer Stamp Duties (ABSD) when buying a second property.

That may well be the case but there can be other better reasons too.

In this blog post, let’s look at how we can also buy new launch condos in a trust and how it is a way of a forced savings plan.

New Launch Condos in Singapore

In Singapore, there are many new launches of private condominiums and landed properties.

These are usually sold when they are not yet built but when they are just a plan and the condos are just but a model in a showroom.

Buying new launch condominiums is a good form of upgrading from HDB and as a form of investment or a form of passive income.

An example of an excellent new launch property in 2019 is the Hyde. Or Watten House condo in 2023.

Watten House Condo is a good buy in 2023

In Singapore, new launches are also called “Building under Construction (BUC)”.

Because the property is progressively being built, the appropriate financing method is also progressive in nature. It is called “Progressive Payment Scheme (PPS)”.

But certainly not to be confused with Singapore Airlines PPS 🙂

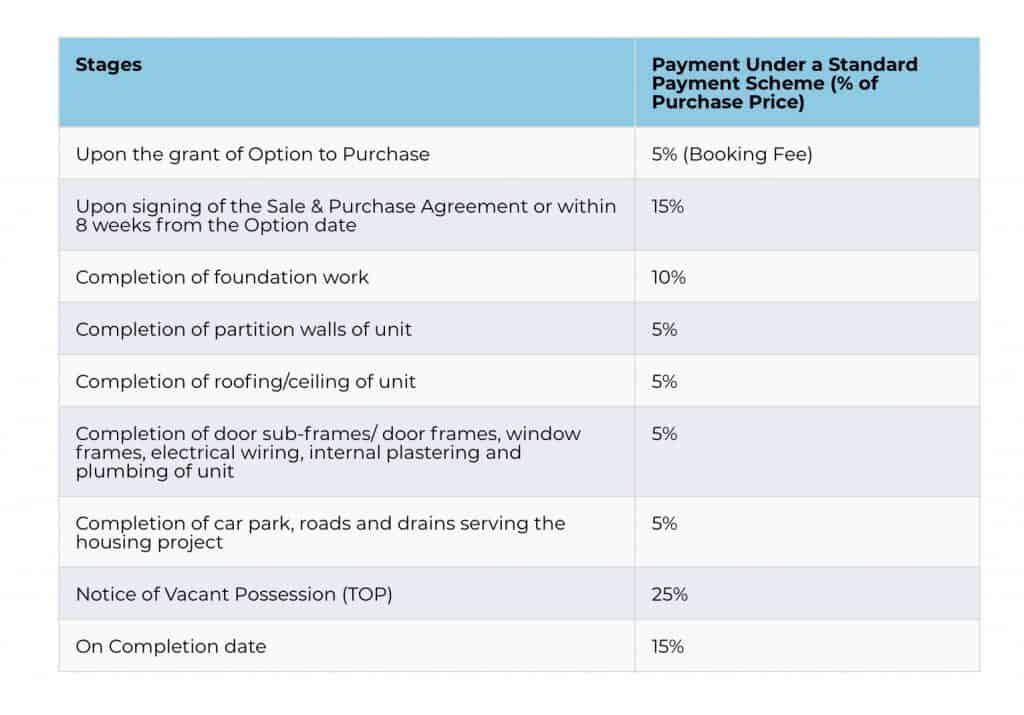

What is the Progressive Payment Scheme

The Progressive Payment Scheme (PPS) is the payment method used for properties that are basically still under development.

Rather than pay for the whole property at one go (as you do with resale completed units), the Progressive Payment Scheme means that you (or your bank) only pay to the developer when certain certified and pre-determined construction milestones are hit.

This chart shows how the payments are made over the life time of a building under construction.

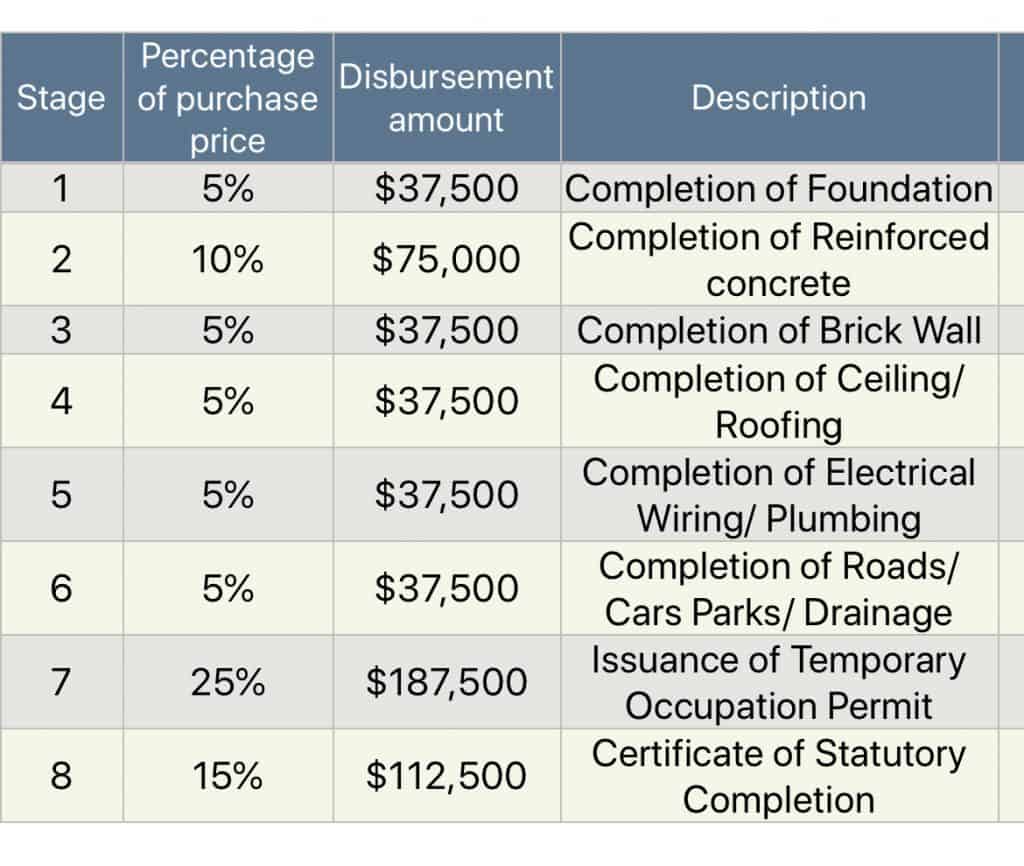

How will the Progressive Payment work for a $750,000 property

I am going to illustrate how the Progressive Payment Scheme works for a $750,000 property.

I am choosing this quantum (which is possible for a one bedroom or a small two bedroom in some areas) because this is the amount that is relevant for our topic for this article. Which is, basically, to buy new launch condos with a trust.

For larger quantum, talk to your friendly real estate agent or use an online calculator.

Here is the progressive payment schedule AFTER the 25% down payment and Buyer’s Stamp Duty (BSD).

That means this chart shows how the payment of the remaining 75% of the $750,000 property is spread out over the “life” of the construction of the condo.

How Does Buying New Launch Condos in a Trust serve as a Saving Plan for you

So let’s talk about buying new launch condo in a trust.

Remember that in the previous post on buying a trust property, that when buying a property for your child, you cannot use CPF nor can you use any bank loans.

So you must use all cash for this property under construction.

Hence for the example above, you will need to pay $750,000 in cash for the condo and also about $17,100 for Buyer’s Stamp Duty.

However, there are several good “features” of the Progressive Payment Scheme that we can look at when buying this $750,000 property for your child under a trust.

Firstly, we are looking at an affordable quantum of $750,000. This usually get a one bedroom or a small two bedroom unit. Which, besides being affordable, is also the right size to rent out as a passive income source. This is because you are probably buying this property for the child for the future and not really going to move into this property upon completion. Hence it makes for a good rental play. The rental will go into the trust. Which will be for the benefit of your children.

Secondly, we are buying a building under construction. Because of the Progressive Payment Scheme, we are only required to make each payment only at each completed milestone. You are not paying for the whole transaction at one time, like in a resale.

Basically, in most new launches, we are looking at each milestone at around 3-6 months between each milestone. In other words, we are looking at making each payment roughly every six months.

This is why we also called this as a forced savings plan. You are being “forced” to pay save $37,500 every six months or so.

Also, the final payment is about one year AFTER temporary occupation permit (TOP). If you are familiar with building under construction, TOP is where you are receiving the keys to the unit from the developer. Because it is a condo, not much renovation are needed to make this unit ready for rental. This means, you are already collecting rental income for almost a year before the final payment.

Finally, besides being a rental play, the completed new launch property will likely be producing a capital gain. When the conditions are right (eg the property market is hot, 5 years is over (why. ask me. 🙂 ), the Rental Yield is no longer attractive and your child has grown up and might want to buy his/her own HDB flat), you can then sell the property for a good price and return all the cash payments AND a profit back to the trust. And then, depending on the terms of the trust, dissolve the trust and you can get back all the monies. These monies will also include the rental the property has collected over the years.

Now is that a good savings plan or not 🙂

What do you think ?

A true life example

Here is a newspaper cutting for someone who has plans to buy properties for his children with small units at new launches.

You can certainly do the same for your children. Start small but do start 🙂

Member discussion